Contents

CEMENT SECTOR ANALYSIS

>Questions we are going to answer

1)What is Cement?

2)Swot Analysis of Cement Sector

3)General Condition of a Cement Sector in the World

4)General Condition of a Cement Sector in Turkey

5)Related Sectors

6)Cost Components and Problems of Sector

7)Porter’s Five Forces Model

8)Future Prospects of Cement Sector

What is Cement?

A cement is a binder, a substance that sets and hardens independently, and can bind other materials together

A cement includes calcium, silicon, aluminium, iron-oxide, calcareous, clay, marn, iron gem.

Clinker is ground to become Portland cement. It may also be combined with other active ingredients or chemical admixtures to produce:

– ground granulated blast furnace slag cement

– pozzolana cement

– silica fume cement

Types of Cement

Portland cement:The most common use for Portland cement is in the production of concrete

Non–Portland hydraulic cements

-Pozzolan-lime cements

-Slag-lime cements

-Supersulfated cements

-Calcium aluminate cements

-Calcium sulfoaluminate cements

SWOT Analysis of Cement Sector

Strengths

Cement is, literally, the building block of the conAlmost every building constructed relies on cement for its foundation

struction sector

The cement business is a $10 billion sector, measured by annual cement shipments

There is also a strong reputation behind the cement sector

Cement is a solid material and consumers rarely have complaints about the product

Regional distribution plants have also made cement widely available to any type of buyer.

Weaknesses

The cement sector is not without its drawbacks

The cement sector relies on construction jobs to create a profit

The cement sector heavily relies on weather

About two-thirds of cement production takes place between May and October

Cement producers often use the winter months to produce and stockpile cement, to meet demand

The cost of transporting cement is high and this keeps cement from being profitable over long distances

In other words, shipping cement costs more than the profit from selling it

Opportunities

One opportunity is the cement sector’s efficiency

The cement sector has recently streamlined its production efforts, using dry manufacturing instead of wet, which is heavier and more time-consuming

The cement sector has also invested about $6 billion in expansion efforts to meet unmet cement needs

Projections show that by 2012, the cement sector will have 25 percent more production capabilities

Threats

The nature of the economy have uncovered a number of threats to the cement sector

The cement sector greatly relies on construction

The current economy has lessened the number of construction jobs, which in turn hurts the cement sector

Kyoto Protocol and EU Environmental Legislation has introduced regulations for the cement sector to cut down emissions

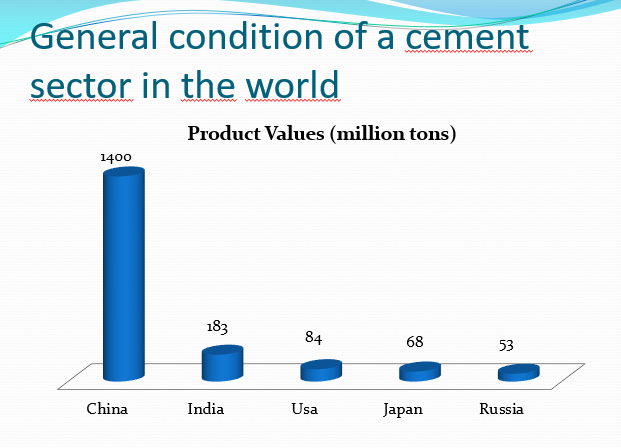

In 2008, world cement production reached 2,87 billion tons

European Cement Union countries produces 11 % of total world cement production

In 2008 and 2009, because of the economic crisis, production of cement is decreased

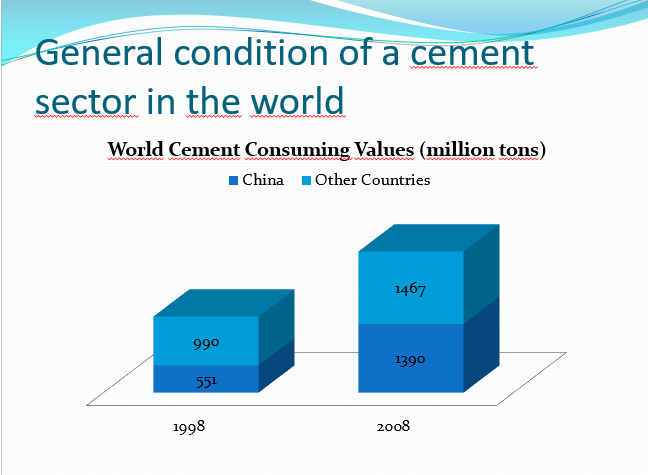

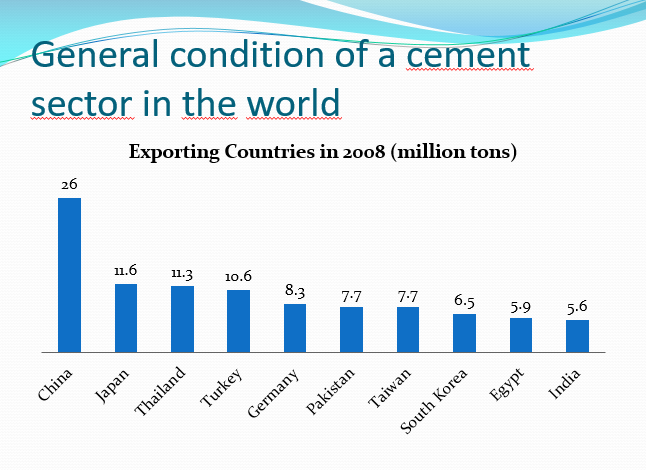

In 2008, exporting value of China was 26 million tons but in 2009, it dropped to 14 million tons and its capacity increased to 1,3 billion tons

It indicates overcapacity problem of a sector

Global economic crisis in 2009, affected mortgage market in USA, after that construction sector and so cement sector are affected

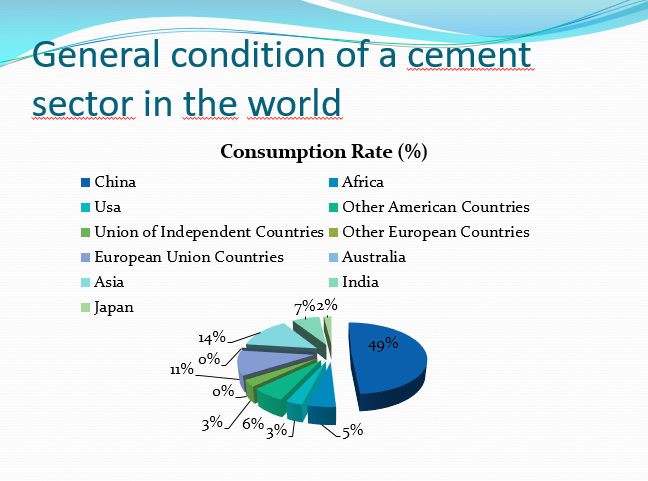

Consumption of cement is decreased mostly in America and Europe continents

Consumption is decreased most in Russia (25%)

Although these decreases, cement consumption increased in Mediterranean Countries such as Libya, Algeria, Syria and Iraq

Turkish cement sector is in the first ten countries in the world

In Europe, Turkey is third in production and fourth in selling cement

In 2009 production reached 54 million tons and capacity reached 90 million tons.

Cement sector is only sector which is not unregistered in construction sector

Demand in cement sector changes according to economic conditions and investment environment in related country and it stagnates the period that there is no expenditures

Especially, the last global economic crisis affected construction and real estate sectors, so demand of cement is decreased

In cement production raw material, auxiliaries, energy and fuel are important cost components

Also transportation is other important component

Especially cost of energy, fuel and transportation demage competitiveness of the cement sector in the market

Turkish cement producers have disadvantages in cost according to the international competitors in the market

Capacity Problem

Because of overcapacity and intensive competition, prices are decreased and sector is in trouble

In 2008 Feb, average cement price was 120 TL, but it decreased 27 percent to 88 TL in 2009 Feb, also in 2010 average price is 85 TL

It is expected that the capacity problem will continue for a while because of stagnation in the market

To solve this problem investments must be planned and controlled

For using all of the current capacity, investment of civil infrastructure and urban regeneration projects must be increased

Transportation

In fact increasing in domestic and international markets, increased production cost affect export in bad manner

The most important factors in the exporting cement is inadequate railways and export ports

Because of the inadequate ports, exports are made by highways

High transportation cost is important barrier in exportation

To solve his problem there must be policies to increase exportation

Ports and logistic projects must be improved

Energy

Especially high petroleum prices affect cement sector badly

Because of low sale prices which is caused by overcapacity, sector is in trouble because of incerasing production cost

There must be fiscal policies in energy costs

Also companies are sensitive about energy efficiency and increase environmental awareness

Also companies are sensitive about energy efficiency and increase environmental awareness

There must be trainings about energy efficiency and cost advantages must be determined

Environmental Regularization

Kyoto Protocol and accordance to EU Environmental Legislation are important problems about environment

In this process sector will have to make high technological investments and establish new treatment plant

For this expenditures and investments finance and timing are main problems

Research&Development

Projects must be developed to decrease gas emissions and energy consumption

It must be provided that sector has to give importance to R&D activities

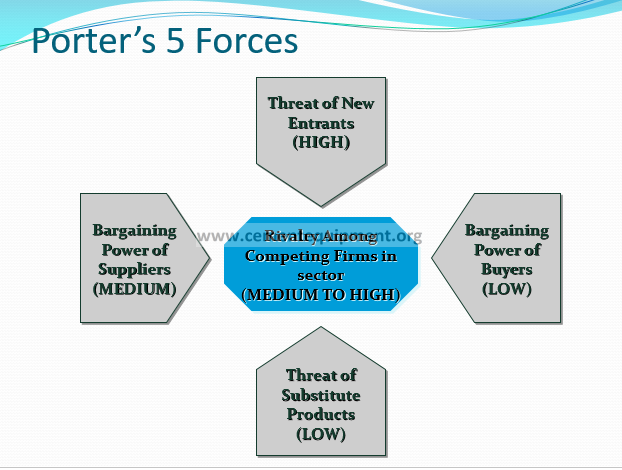

Porter’s 5Forces-Barriers to Entry

There are no barriers to entry

But if you want to build a cement factory capital cost is high (approximately 130 million dollars to build 3500 tons/days capacity)

The main consumer is housing markets

Housing is now booming as a part of the remittances is being used for construction of houses

Commercial banks with liquidity are finding housing sector potential area for lending

Infrastructure is the another segment of cement sector

Cement demand in emerging economies is much higher than developed countries where the demand has reached a plateau

Licensing of main reserves is controlled by government

The shortage of a raw material remain a concern

Transportation and packaging suppliers can affect bargaining power so backward integration can be used

Gypsum plaster is a good substitue for construction purposes

Gypsum plaster is also useful in construction in regions of extreme cold and hot climate for isolation

Existing firms are trying to expand their capacity

Government enforce the improvement quality of the cement and rivalry by the anti-trust laws

Competition Board is analyse the sector, for mergering, acqusition, and price statement activities

Future Prospects of Cement Sector

As it is mentioned before global economic crisis affected construction sector so cement sector is also affected

The world have experienced a recession in demand in 2009

Turkey also affected by the recession and declines in domestic consumption was observed

170 million tons in the entire world experienced an increase in capacity, and this has created excess demand

Experienced decline is foreseen in the coming years, increases in capacity, capacity increases are expected to be provided by the majority of developing countries

Losses in the demand recovery is expected in the coming years, in Europe such a recovery is not expected in the short term

The investment in the sector is thought to increase in the United States and Russia

Cement consumption in the two countries share most of the India and China have shown differences in the predictions for 2010, India’s growth potential is expected to be higher than China’s